US Markets

From sandstorms in Riyadh to headwinds in Rome, escalating risk has effectively capped the recent swell in US Treasury yields, while the combination of Federal Reserve policy tightening and increasing debt supply should keep the trapdoor from giving way. But none the less, market participants will jostle between US growth momentum and the ever-threatening and escalating geopolitical risk, that could trigger a more significant flight to safe-haven currencies and assets.

US equity markets struggled across the finish line on Friday as investors contiued to take profits after morning gains gave way when a report showed U.S. home sales fell for the sixth month in a row. US housing growth continues to disappoint on familiar themes and remains one of the few red lights and the most significant drag on the US economy.

China Markets

Although local Asia sentiment remains poor, the SHCOMP staged an impressive reversal of Friday after China rolled out a series of speakers and rule changes to stabilise markets, but the pace of reversion does suggest it was aided on by state-owned funds to add some vim. But Chinese markets remain under pressure from every economic angle leaving more than a few investors extremely sceptical Friday’s recovery will have lasting legs.

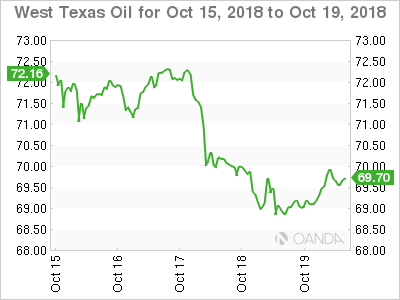

Oil Markets

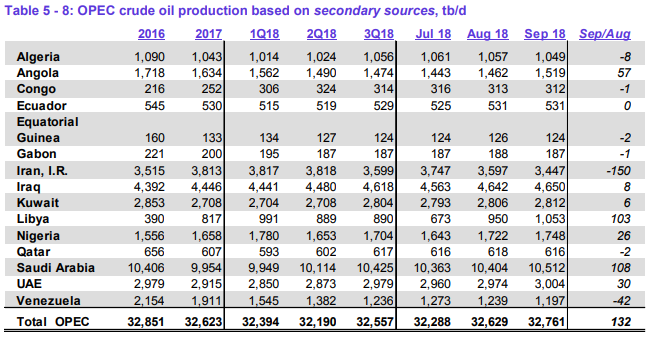

It should be a hectic week ahead in oil markets anticipating colossal participation amidst escalating headline risk this week . Bullish sentiment is clearly under pressure as oil traders search for the next equilibrium.

Brent crude oil probed back above the $80 per barrel on Friday after China reported record refinery throughput for September.Reuters But the critical benchmark still closed below that technically essential and psychologically significant level. ($80 per barrel)

West Texas Intermediate crude oil followed stronger performances in the Brent market, but like Brent, closed below a key level, $70 per barrel, which is a significant fail for bullish sentiment

In China, higher seasonal demand and suspected stockpiling are occurring, while similarly the US and the OECD continue building stockpiles ahead of potential supply disruptions this winter. But China demand is also surging due to Beijing ‘s enormous infrastructure projects and spends which are being used to stimulate the economy and is beefing up Oil demand.

However, concerns about demand growth slow down along with the prospect of more barrels coming online has triggered a sizable reduction in bullish markets structures, the difference between bets on higher prices and wagers on falling priced — dropped 14 per cent to 242,855 futures and options in the week ended Oct. 16, according to the U.S. Commodity Futures Trading Commission.

But there’s a loud level of headline noise that seems to pop up like clockwork, where on the one hand views suggest OPEC can quickly cover the Iran shortfall while conspicuously well-timed documents continue to surfacing claiming that OPEC and its allies are having difficulty boosting production by 1 million bpd as it had promised in June. Sifting through the market noise will present its challenges none the less.

From various industry insider reports, Iran exports have fallen from 2.2- a million barrels per day (m b/d) in 1H’18 down to an expected 1.5-m b/d in October. Saudi Arabia has reportedly ramped production to 10.7-m b/d though. They could go to 11-m b/d and draw down 0.5-m b/d from inventories or even more if needed. (3-m b/d just boosted Saudi export capacity at Aramco’s Red Sea Yanbu terminal. Ras Tanura capacity is well above current export levels.) And Russia still has ~0.2-m b/d spare capacity to reach 11.5-m b/d.

According to industry reports, Canada’s crude production was ~4.6-m b/d in August, with Jan-Aug growing ~280-k b/d y/y, even with Syncrude upgrader problems, which has since recovered. Oversupply and US refinery maintenance have put WCS and Syncrude into a massive discount WTI pipeline bottlenecks meaning more and more WSC needs to be shipped by rail with new longer-term rail shipping contracts agreeing to at ~$20/bbl to the USGC

And with Trump’s acknowledging that Saudi Arabia’s findings behind the Khashoggi death were credible, this could offer more opportunity for the US administration to pressure the kingdom to tap its spare capacity resources before the Iran sanctions take effect in November. So, there will be an intense focus on the Saudi Royal family’s relations with the Whitehouse this week, while US Congress will face increasing pressures to block all arms sales and deliveries. All the while global business leaders continue to shun “Davos in the Desert.”

US-Saudi relationships are vital to maintaining peace in the middle east and must continue, however, the Khashoggi case will give the US leverage and which will likely cause Saudi Arabia to increase oil production if possible. But you know this is not going to leave the headlines anytime soon as most everyone considers the official Saudi explanation as a complete fabrication.

While the supply-demand equilibrium remains fragile, the anticipated impact from Iran sanctions is diminishing as prompt Brent remains in good short-term supply despite growing uncertainty about supply disruptions continue to build down the road.

Gold Markets

Investor sentiment is much-improved from even a week ago on increased portfolio hedges against more sustained equity market drawdown which over the short term, should give rise to haven demand and boost Gold prices.

But China has rolled out some rule changes to stabilise markets. And while the longer-term effects from these changes amount to little more than putting a band-aid on a broken leg, the generally usually work and have some influence over the short term. Since China equities are deep in oversold territory, there is lots of room for a bounce in local markets which has clipped momentum in Gold markets as even headlines around Brexit, and the Italian budget was more positive heading into the weekend. heading into the weekend although most traders remain a bit cynical on those fronts

While the upcoming US election will offer up many challenges on US political risk front and support Gold, ultimately however past Nov 6 USD and Fed hiking cycle are likely back in the driver’s seat for bullion pricing. While mainly priced in, the USD could strengthen ahead of December rate as higher US interest rates and a stronger USD could discourage gold investors from pushing the envelope higher unless of course, the equity market rout continues.

Currency Markets

From sandstorms in Riyadh to headwinds in Rome, escalating risk has effectively capped the recent swell in the US in Treasury yields, while the combination of Federal Reserve policy tightening and increasing debt supply should keep the bottom from giving way. But none the less we will bond, and currency traders are left to jostle between US growth momentum and tightening global risk, that should trigger a more significant flight to safe-haven currencies and assets.

Last weeks FOMC minutes reaffirmed the Fed’s hawkish lean and should keep the dollar supported. Markets remain in pins and needles of the Italy budget and Brexit stalemate, but with equity markets volatility on the rise, traders will continue to assess China policy adjustments on Friday to see if the moves will have a sticky effect.

Traders will soon factor in US midterm elections where the tail risk clearly, is a Democratic sweep. Mind you; its anyone’s guess just how economically active GOP tax cuts will be in 2019 while facing a massively ballooning debt. But it is while is more clear-cut that a Blue Wave tsunami would dent market sentiment and likely push the dollar lower

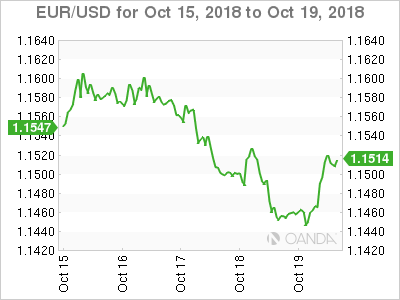

The Euro

So far ECB policymakers have remained somewhat mute on Brexit, but one would think this divorce will not play out pretty for either the EU or UK economies which might influence ECB policy guidance. But EURUSD is back above 1.1500, reflecting quietening in alarm bells over equities & Italy. Moody’s finally cut Italy’s ratings to Baa3 as expected. Italy’s banks are vulnerable because of the high proportion of the country’s bonds they own, but this was widely expected so no major surprise.

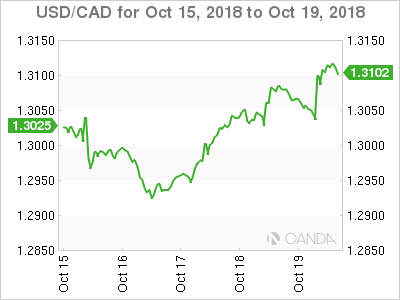

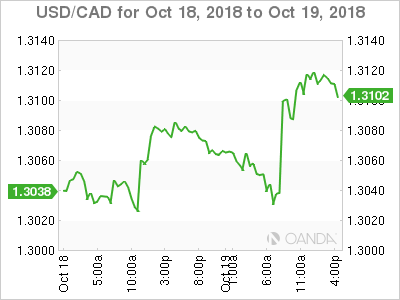

The Canadian Dollar

The CAD miss on CPI has overwhelmed whatever remnants of bullishness I had in the CAD. The shocking miss on the CPI has shattered my confidence on next week’s BoC. Given there are no significant data releases between now and the BoC meeting, its time to stop being so unabashedly bullish on the loonie.

Australian Dollar

There were around $A10B of Australian government bonds redemption on October 21 and given much better yields away, unless so governed to buy Australian Bonds, most of those maturing investments likely funnelled into US or other much higher yielding bonds. Thus, the AUD is holding up well despite a lot of selling pressure last week and could outperform this week provided China volatility continues to ease after mainland regulators policy tweaks on Friday.

Been avoiding trading AUD vs the USD like the plague but given shifting sentiment on BoC policy next week, the long AUDCAD trade could see some appeal early this week.

On the energy front, multiple news sources have confirmed that Australia’s colossal and much delayed Ichthys liquefied natural gas (LNG) plant has started shipments in recent weeks. But comes at a favourable time and could offer some much-needed respite to Australia’s dwindling heavy sweet crude oil production.

The Malaysian Ringgit

It still feels like risk off but with a less weak Yuan and the monetary policy easing story in China playing out well on the SHCOMP. While the mainland equity recovery was positive on the surface, other regional bourses barley blinked as the China market reversal was little more than it a short covering.

In what could best be described as hope for the best but prepare for the worst. Malaysia slashed its economic growth targets and deserted its plans to balance its budget by 2020, not exactly a ringing endorsement for the financial in Malaysia. And with capital gains taxes and other consumption taxes on the horizon, it’s not to difficult to figure out why Malaysia equity markets remain under pressure.

The combination of macro risk off as well as on-shore danger around the upcoming budget will keep the Ringgit trading defensively.

The leak on oil prices notwithstanding, regional risk sentiment remains ever so fragile as any sliver of optimism from US earnings gave way to that reality that trade tension and geopolitical unrest continues to gurgle. There were around $A10B of Australian government bonds redemption on October 21 and given much better yields away, unless so governed to buy Australian Bonds, most of those maturing investments likely funnelled into US or other much higher yielding bonds. Thus, the AUD is holding up well despite a lot of selling pressure last week and could outperform this week provided China volatility continues to ease after mainland regulators policy tweaks on Friday.

Been avoiding trading AUD vs the USD like the plague but given shifting sentiment on BoC policy next week, the long AUDCAD trade could see some appeal early this week.