Authored by Adam Taggart via PeakProsperity.com,

When it goes up, prices go down. It’s going up…

This is a revisitation of a report I wrote back in late 2016, predicting the imminent end of zero-bound interest rates and warning of the downward pressure that rising rates, mathematically, must place on today’s elevated asset prices.

Since the publication of that report, interest rates have indeed vaulted higher. Look at how the 3-month US Treasury yield has exploded since the start of 2017:

A Little Background

When I was fresh out of college in the mid-90s, I landed a job at Merrill Lynch. I was an “investment banking analyst”, which meant I had no life outside of the office and hardly ever slept. I pretty much spoke, thought, and dreamed in Excel during those years.

Much of my time there was spent building valuation models. These complicated spreadsheets were used to provide an air of quantitative validation to the answers the senior bankers otherwise pulled out of their derrieres to questions like: Is the market under- or over-valuing this company? Can we defend the acquisition price we’re recommending for this M&A deal? What should we price this IPO at?

Back then, Wall Street still (mostly) believed that fundamentals mattered. And one of the most widely-accepted methods for fundamentally valuing a company is the Discounted Cash Flow (or “DCF”) method. I built a *lot* of DCF models back in those days.

I promise not to get too wonky here, but in a nutshell, the DCF approach projects out the future cash flows a company is expected to generate given its growth prospects, profit margins, capital expenditures, etc. And because a dollar today is worth more than a dollar tomorrow, it discounts the further-out projected cash flows more than the nearer-in ones. Add everything up, and the total you get is your answer to what the fair market value of the company is.

The Weighted Average Cost Of Capital

The DCF approach sounds pretty straightforward. And it is. But it’s still much more of an art than a science. Your future cash flow stream is entirely dependent on the assumptions you bake into the model. The difference between a 5% or 15% assumed EBITDA compound annual growth rate becomes huge when projecing over 10+ years.

But one assumption in the model has far more impact on the final valuation number than any other. And it has nothing to do with the company’s projected operations.

Recall that the DCF approach projects out the expected future cash flows, and then discounts them (back to what’s called a “present value”). This raises a critically important question:

At what rate do you discount these future cash flows?

Well, to address this, you need to ask yourself a few questions. How will the company be financing itself? It will need to deliver an acceptable return to both its stockholders and bondholders. What kind of return can investors get out in the market for a similar investment? If they can get a better expected rate of return, or similar return with less risk, they’ll put their money elsewhere.

Enter a calculation known as the Weighted Average Cost Of Capital (or “WACC”). Again, without getting too technical on you, the WACC looks at how a company is capitalized (what % with debt, what % with equity) and what blended annual rate of return the investors who contributed that capital expect. Once you’ve calculated the WACC, you put that number into your DCF model as the annual discount rate and — Voilà! — your model spits out the present value for the company.

It’s All About The “Risk Free” Rate

So, to recap:

-

Companies (really, any asset with an income stream) are valued off of the present value of their discounted future cash flows

-

This present value is highly dependent on the discount rate used

We just talked about how the WACC is commonly used as the discount rate (or, at least, its foundation). So how is the WACC calculated?

Here’s its formula (Don’t let it scare you; I’m not going to get all mathy on you here):

I want to point your attention to two important factors in this equation: the cost of equity (re) and the cost of debt (rd). The size of these variables has a big impact on the final number calculated for the WACC.

Re, the cost of equity, is made up of two components: the market’s current “risk free rate” + the “equity premium” that investors demand on top of that to hold stocks, which have more risk. Most folks use the current yield on the 10-year US Treasury bond as the risk free rate (which is now over 3%).

Similarly, rd, the cost of debt, has two components: the market “risk free rate” + the premium that the company’s bondholders are charging to hold debt riskier than a Treasury bond.

Note that the “risk free rate” is a critical component of both re and rd.

So, as interest rates (i.e., 10-year Treasury yields) rise, the cost of equity goes up and the cost of debt goes up, too.

Why is that so important? Glad you asked…

The Future Of Rising Rates (And Falling Asset Prices)

Most reading this are aware that we’ve been living in a falling interest rate environment for most, if not all, of our adult lives. And since the 2008 financial crisis, interest rates were held down at essentially 0% (or even lower) by the world’s central banks:

While not the only reason, this decline in interest rates has been a huge driver behind the tremendous rise in valuations across assets like stocks, bonds and real estate over the past 30-odd years.

Which begs the question: What will happen to asset prices now that interest rates have started rising again?

Well, as I hope the above lesson on the Weighted Average Cost Of Capital hammered home, when the core interest rate rises, both the cost of equity and the cost of debt go up. Mathematically, this increases the WACC used as a discount factor, thereby reducing the present value of future cash flows.

Or in layman’s terms: When interest rates rise so does the WACC, which mathematically makes valuations fall.

In my original report back in December 2016, I penned the following:

Now, we only need to care about this if we’re worried that interest rates will start rising. Maybe the central banks have everything under control. Maybe we’re at a “permanent plateau” of sustainable zero-bound interest rates.

Well, we now know the answer: It’s time to worry.

Remember how the “risk free rate” used in calculating the WACC is often the 10-year Treasury bond yield? Since writing the above, the yield on the 10-year Treasury has nearly tripled, and has recently cracked above the much-feared 3% level, the milestone at which many analysts have predicted it would cause a major correction in the financial markets:

It has taken a while for the higher cost of capital to ripple through the system, but the repercussions are now becoming apparent.

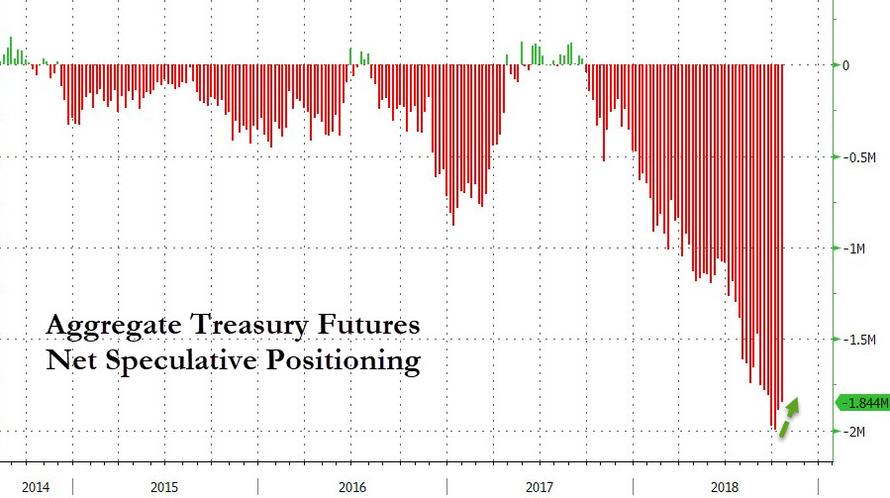

Bonds have been in sell-off mode the longest, pretty much since since l gave warning at the end of 2016:

The housing market, which is sensitive to interest rates given the see-saw mathematical relationship between mortgage rates and real estate prices (i.e., higher rates = lower prices, all else remaining equal), has started cooling off after an eight year bonanza. As we’ve recently detailed in our report Trouble Ahead For The Housing Market, the most popular formerly red-hot markets are all showing signs of stalling/declining prices.

Nationwide, versus last year, mortgage applications have tanked 15% and home refinance loan applications have declined 34%. Mortgage rates are now the highest they’ve been since 2011 — but of course, houses are substantially pricier than they were then, too. Affordability is now a huge issue increasingly restricting the pool of potential buyers, as starkly presented in this CNBC video:

Meanwhile, the stocks of homebuilding companies have been selling off hard since the 10-year Treasury cracked above the psychologically-important 3% threshold:

Speaking of stocks, many pundits have been attributing much of last week’s market plunge to the bite today’s higher interest rates are starting to have across the economy:

The biggest change has been an acknowledgement that rising interest rates could cool a strong U.S. economy and also put a dent in corporate earnings. The combination of the Federal Reserve hiking short-term rates last month and another increase expected in December, coupled with a spike in the 10-year U.S. government bond to a seven-year high has made stocks less attractive compared with lower-risk bonds.

Low rates and cheap money resulted in a flood of money into stocks in recent years, as people searched for bigger returns.

But now financial conditions are getting tighter.

“The wave of money that was moving into the market is now reversing,” says Savita Subramanian, head of U.S. equity strategy at Bank of America Merrill Lynch. “As liquidity is withdrawn from the market, it amplifies market volatility” and price swings.

Higher borrowing costs also make it tougher for Americans to afford houses and buy cars on credit, analysts say.

(Source)

Rising interest rates are quickly creating a political snafu. President Trump, who has enthusiastically claimed credit for the market rally that ensued after his election, is now lambasting new Federal Reserve Chairman Jerome Powell (whom Trump appointed) for departing from his predecessors’ path of quantitative easing (i.e., bringing interest rates to historic lows).

Trump is now accusing Powell of having “gone crazy“, going as far to claim that “The Fed is my biggest threat“:

Trump Blames ‘Out of Control’ Fed for Rout But Says He Won’t Fire Powell (Bloomberg)

President Donald Trump said he won’t fire Federal Reserve Chairman Jerome Powell but blamed an “out of control” U.S. central bank for the worst stock market sell-off since February.

Trump also told reporters in the Oval Office Thursday morning that he knows monetary policy better than the Fed’s leaders and continued criticizing them for interest-rate increases.

“The Fed is out of control,” Trump said. “I think what they’re doing is wrong.”

The president added that the Fed’s interest rate increases are “not necessary in my opinion and I think I know about it better than they do.”

Is this a sign Trump will pressure the Fed to reverse path, possibly even replacing Powell? Or is this just deliberate theatre on his part to position Powell as the fall guy should a full-blown market correction be in the cards?

Either way, these higher rates were inevitable and eminently predictable by the administration. Back when I wrote the original version of this report in late 2016, Trump’s newly-selected Treasury Secretary Steve Mnuchin clearly declared the following:

“We’ll look at potentially extending the maturity of the debt, because eventually we are going to have higher interest rates, and that’s something that this country is going to need to deal with.”

(Source)

Indeed, like it or not, we’re now being forced to learn how to deal with higher interest rates.

Prepare Now

The conclusion from all the above? Get ready to live through the new era of rising interest rates. It’s going to be unfamiliar territory for all of us…

What will likely happen? The unrelenting upward march in asset prices we’ve enjoyed over the past several decades is over. People won’t be able to pay as much for stuff because the financing costs will be higher.

Falling asset prices should be in the cards. We’ve already been seeing that with bonds, and housing and stocks look like they are finally following suit. The higher rates go, the farther the fall should be.

The Fed will be in a tough spot as this unfolds. Right now, the Fed is in quite a box after years of habituating the market to ZIRP. Powell seems serious about continuing to raise rates as far as the financial markets will tolerate, provided he can do so without killing the economy — which is a big “if” at this point. There’s a lot of precedent for this; historically, the Fed’s interest rate has usually followed the market vs leading it. The Fed wants to gain some maneuvering room to drop rates at some point in the future if it feels it needs to.

At some point, if we risk entering a full deflationary rout, the world’s central planners may well indeed pull out an arsenal of tricks similar to what we saw following the 2008 crisis. We may eventually see liquidity-injection programs so extreme that hyperinflation becomes a valid concern. But that time is not now.

For now, we recommend the following:

-

Get out of debt. Especially variable rate, non-self-liquidating debt (credit cards being a great example). As we’ve said many times, in periods of deflation, debt can be a stone-cold killer.

-

Read the Financial Capital chapter from our book Prosper! (we’ve made it available to read for free here).

-

Read our primer on hedging.

-

Talk with our endorsed financial adviser (again, free of charge) if you’re having difficulty finding a good one to discuss this topic with. Be sure to have positioned your financial portfolio to take into account the risks to stocks/bonds/etc raised here.

And put today’s rising interest rates to work in your favor. If you have substantial cash savings, consider putting them in short-term T-bills using TreasuryDirect, which now yield between 2.14-2.45%. That’s over 30x what the average bank savings account is currently yielding. To learn more about this program, read our (free) report here.

The post It’s Not The Economy, Stupid; It’s WACC! appeared first on crude-oil.news.

(@JackPosobiec)

(@JackPosobiec)