Bloodbath in Markets as Trump Points Finger at the Fed

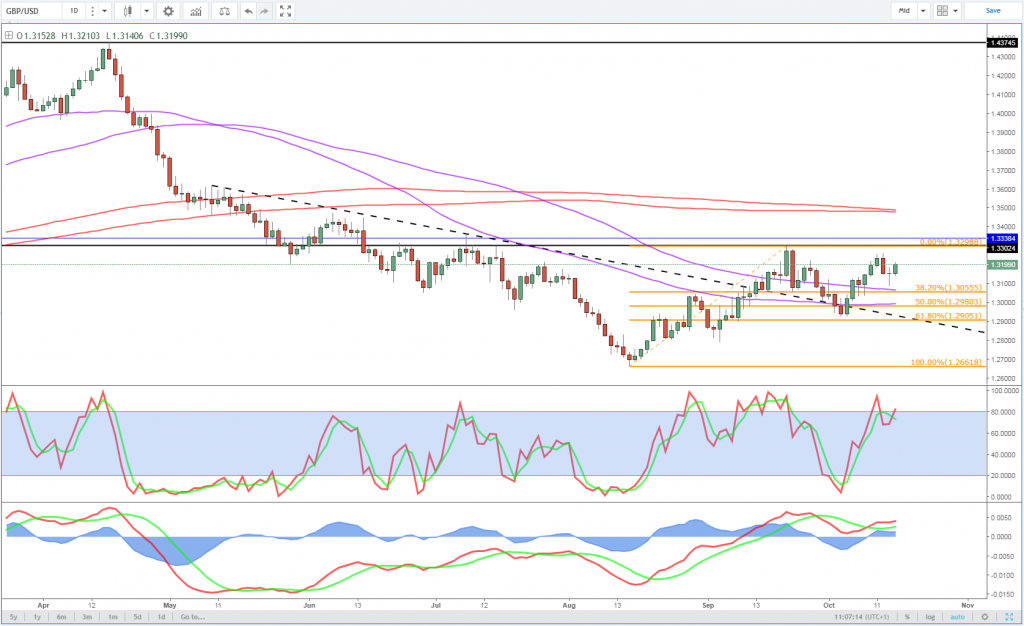

European stocks are set to become the latest casualty in the global sell-off that has rattled markets over the last 24 hours, as investors worry about the potential for a sharper correction on the back of rising bond yields.

It’s been something of a bloodbath overnight, as investors saw what occurred in the US – despite there being no clear catalyst for such a move - and dashed for the exits as fears grow that global risks are mounting and the bill is coming due. While people are naturally pointing to the bond market to explain the sudden panic – most notably Trump who’s been laying the groundwork for blaming the Fed for the last couple of months – I wonder whether the underlying risk in the markets for some time has left market primed for a correction and investors have simply fled at the first sign of danger.

Trump was extremely quick to point the finger of blame at the central bank for raising rates too quickly, but as the CPI data is expected to show today, inflation is running above target despite its actions and the absence of more rate hikes could accelerate that. As is to be expected, Trump is not going to want to accept any responsibility himself for huge tax reforms that provided significant stimulus in an already hot economy, forcing the Fed to hike faster than they may have wanted, or for creating risk in the markets by starting a trade war with China, but that is what is playing out here.

There is the potential for this to be nothing more than a brief shock that markets quickly recover from but the proximity to the mid-term elections in the US could make it problematic for Trump if it turns into more. That more than likely explains why Trump has been laying the groundwork in recent months, in preparation for such a scenario so the seed of blame has already been planted, enabling him to quickly come out on the attack as he has.

Asia Market Update: Worst case scenarios abound

Oil traders lock in profits as sell-off takes hold

It’s not just equities that have suffered the wrath of the bond sell-off, oil bulls also appear to have been run over in the process, with Brent and WTI falling a few percent on Wednesday and extending those losses today. Oil has been scaling long-term highs in recent months and attracting a lot of attention as the US sanctions on Iran prepare to come into effect.

The sell-off on Wednesday and today has prompted some profit taking in oil markets, which should prove temporary as long as the broader sell-off doesn’t worsen too dramatically. It will be interesting to see how quickly traders look at the sell-off in oil and seize the opportunity to buy the dips in an asset that was widely seen as being very bullish only a week ago. Of course, if the recent selling is a sign of more worrying weeks and months to come then you would expect oil prices to suffer as well, particularly if the selling is preceding an anticipated slowdown in the global economy which naturally affects demand.

Pace of equities’ declines slows as Asia mulls Wall Street weakness

Bitcoin status as “gold 2.0” falters as cryptos caught up in selling

The sell-off also appears to have stretched to more exotic instruments, with bitcoin neither displaying the qualities one would expect of gold 2.0, as it has been touted as by some cryptocurrency enthusiasts, or simply escaping relatively unscathed as a new and relatively uncorrelated asset. This truly is a widespread sell-off and anything perceived as a risky asset has been in the firing line. What will be interesting is whether this will be enough to force bitcoin below $6,000 which has proven to be something of a floor for the crypto on numerous occasions this year.

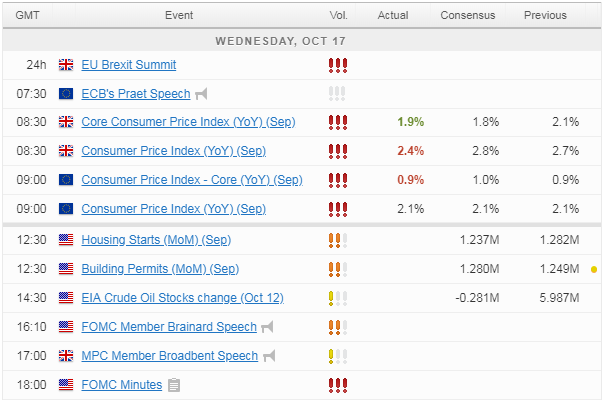

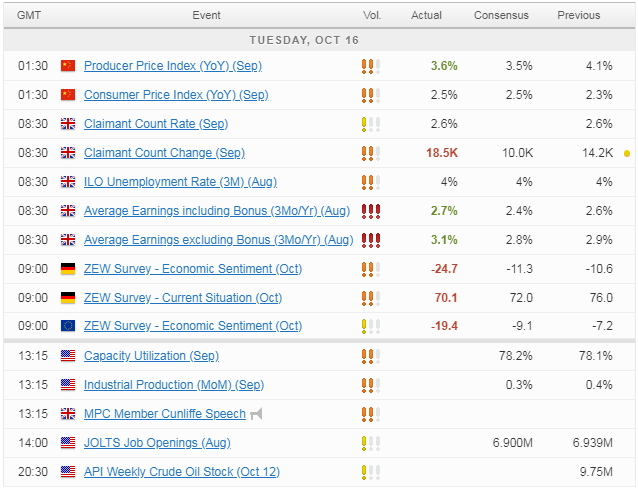

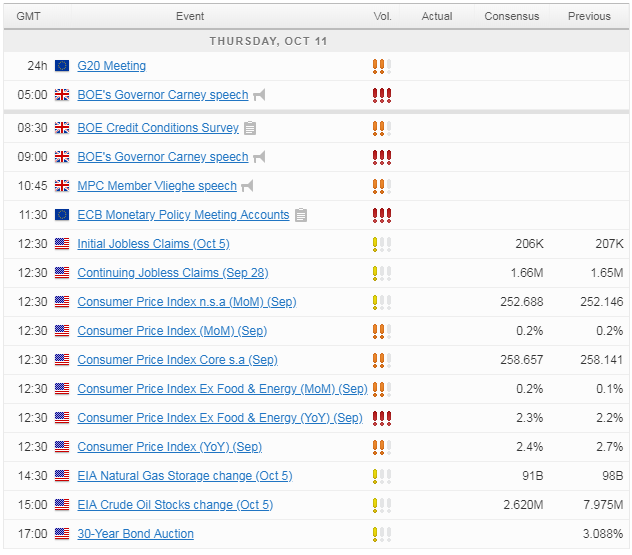

Economic Calendar

For a look at all of today’s economic events, check out our economic calendar.